Deal Talk

March 19, 2025

Easy Trips, Without Cash: Exploring Easemytrip’s Cashless Foreign and Domestic Share Swaps

INTRODUCTION

A recent trend coming up in the market is utilizing

non-cash share-swaps for the purpose of acquisitions

and investments. This structure can be utilized

for the purposes of acquiring an Indian entity or

an overseas entity. In case of a share swap, an

acquirer acquires the shares of another company

(either through a primary or secondary acquisition)

and as consideration for the acquisition, the acquirer

issues its own shares to the other company / selling

shareholders of such other company (“Share

Swap”).

Easy Trip Planners Limited (“EaseMyTrip”)

is currently using this strategy for acquiring stakes

in three companies – Pflege Home Health Care

Centre LLC (“Pflege”),

Jeewani Hospitality Private Limited (“Jeewani”)

and Planet Education Australia Pty Ltd (“Planet”).

Everything was going smoothly, until recently when

Stakeholders Empowerment Services (“SES”)

released a report advising shareholders to vote

against the resolution of EaseMyTrip to issue shares

on preferential basis for the acquisition of Pflege,

Jeewani and Planet.

The baffling question is – why did SES

oppose this move?

In this edition of Deal Talk, we discuss the

complex Share Swap structures adopted by EaseMyTrip

for the aforesaid acquisitions and along with considerations

to keep in mind while structuring such share-swap

acquisitions and why did SES oppose the resolutions.

EASEMYTRIP’s ACQUISITIONS

As per publicly reported information, EaseMyTrip

is planning the following acquisitions in 2025:

Pflege:

Pflege is a limited liability company registered

in Emirate of Dubai in accordance with the provisions

of U.A.E Commercial Companies Law No (2) of

2015 and Law No. (13) of 2011 and operating

under licenses issued by Department of Economy

and Tourism with Home Health Care Center and

Dubai Health Authority. Pflege is a pioneering

company engaged in medical tourism and actively

assists patients in Indian subcontinent, Turkey,

Thailand, Singapore and Malaysia.

Jeewani:

Jeewani is a private limited company incorporated

in India and engaged in the business of construction,

development and operation of hotels.

Planet:

Planet is an Australian company engaged in the

business of international student recruitment,

international student placement, coaching of

various entrance tests like IELTS, TOEFL, GMT,

GRE, SAT, etc. for international education.

Planet is also engaged in opening of educational

institutions for coaching of the aforementioned

tests, student accommodation services, overseas

student health insurance, education loan assistance,

student travel services and forex assistance

services.

|

S. No

|

Target

|

Documentation

|

Deal Structure

|

|

1

|

Pflege

|

Share Purchase Agreement and Investment Cum Shareholders’ Agreement dated December 6, 2024

|

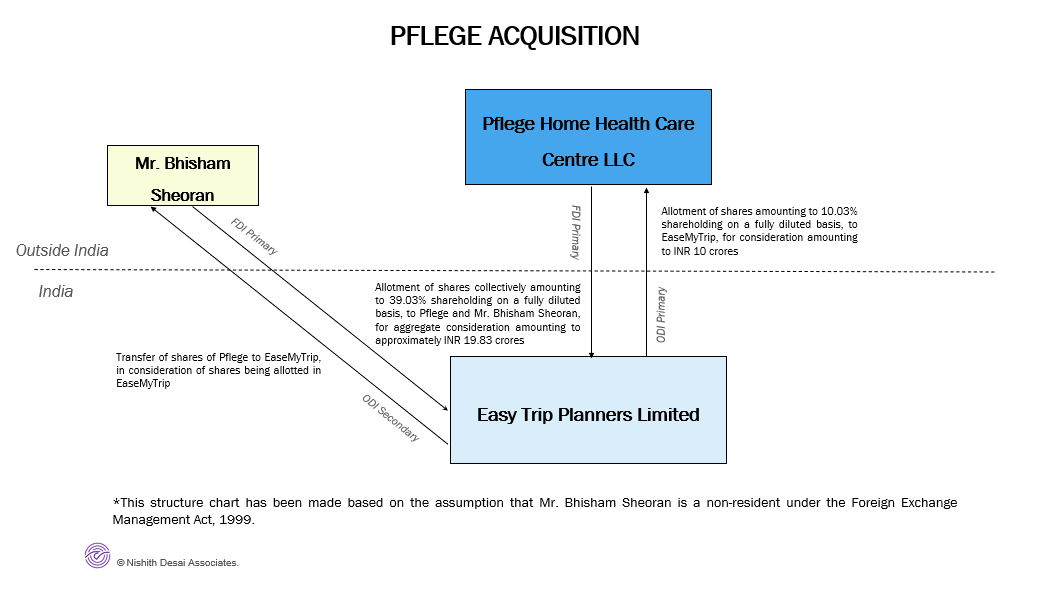

EaseMyTrip is acquiring 49.03% shareholding of Pflege (i.e. 176 shares) through a mix of secondary acquisition and primary investment for a total of INR 29,83,05,000 (Indian Rupees Twenty-Nine Crores Eighty-Three Lakhs and Five Thousand).

A total of INR 19,83,05,000 (Indian Rupees Nineteen Crores Eighty-Three Lakhs and Five Thousand) will be paid through preferential allotment of its own shares to the shareholder, Mr. Bhisham Sheoran, who would in turn sell shares corresponding to 39% shareholding of Pflege to EaseMyTrip.

The remaining INR 10,00,00,000 (Indian Rupees Ten Crores) would be invested (through preferential allotment of EaseMyTrip shares) into Pflege as a primary investment, which would correspond to 10.03% shareholding of Pflege on a fully diluted basis.

(such acquisition by EaseMyTrip, the “Pflege Acquisition”).

|

|

2

|

Jeewani

|

Share Subscription Agreement and Shareholders’ Agreement dated December 6, 2024

|

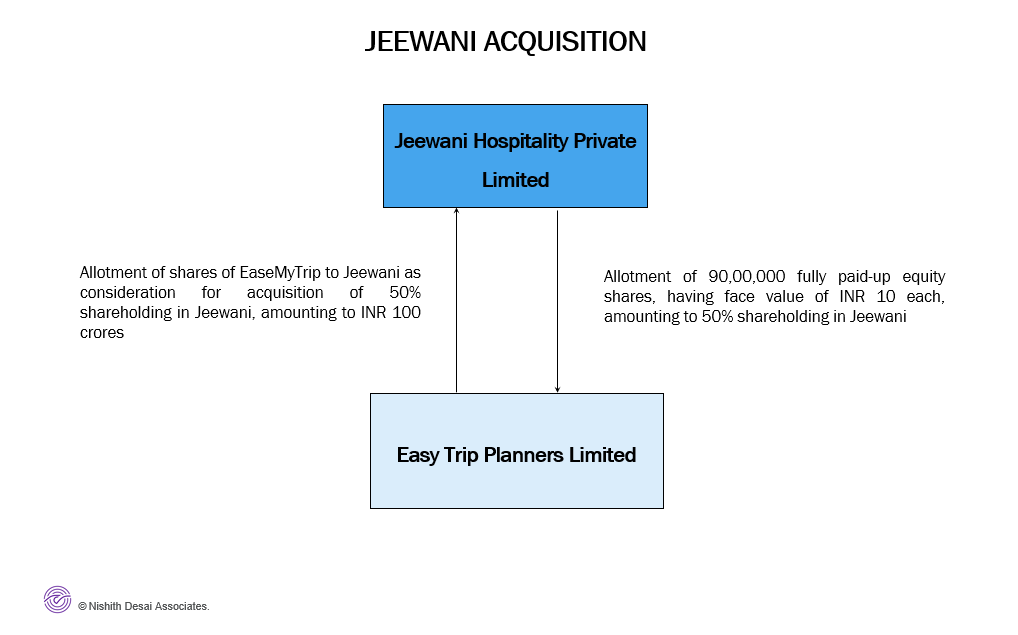

EaseMyTrip is acquiring 50% of Jeewani for a total consideration of INR 100,00,00,000 (Indian Rupees One Hundred Crores) which shall be paid through preferential allotment of its own shares of EaseMyTrip.

The entire investment by EaseMyTrip in Jeewani will be in the form of primary investment into Jeewani. EaseMyTrip will be acquiring 90,00,00 (Ninety Lakh) fully paid-up equity shares of face value of INR 10 each of Jeewani.

(such acquisition by EaseMyTrip, the “Jeewani Acquisition”).

|

|

3 |

Planet

|

Share Purchase Agreement and Shareholders’ Agreement dated October 11, 2024

|

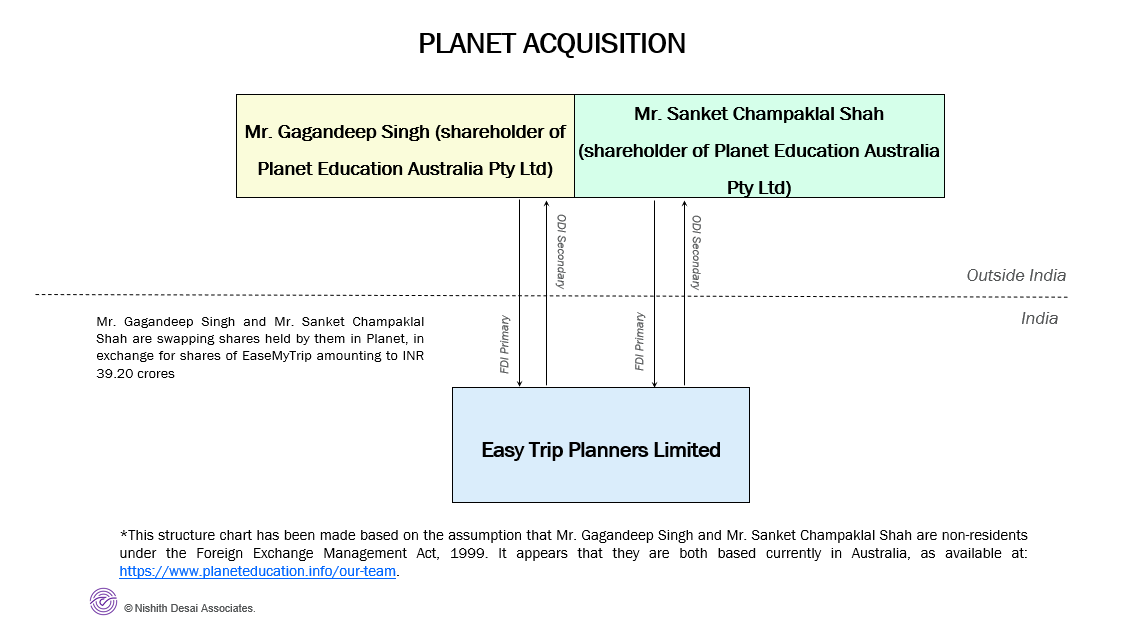

EaseMyTrip is acquiring 49.03% of Planet for a total consideration of INR 39,20,00,000 (Indian Rupees Thirty-Nine Crores and Twenty Lakhs), which shall be paid through preferential allotment of shares of EaseMyTrip.

The entire consideration will be provided to two selling shareholders of Planet: Sanket Champaklal Shah and Gagandeep Singh.

(such acquisition by EaseMyTrip, the “Planet Acquisition”).

|

Interestingly, EaseMyTrip’s primary motivation

to undertake each of the above acquisitions stems

from a desire to further diversify and inorganically

expand their existing business operations globally.

A structural representation of the Share Swaps

are as follows –

(i)

Pflege

Acquisition

(ii)

Jeewani

Acquisition

(iii)

Planet

Acquisition

IDENTIFYING THE UNDERLYING SHARE

SWAPS

Before we delve into the legal considerations

that may have been relevant to each of these acquisitions,

let us identify the underlying Share Swaps in each

of these deals –

1.

Pflege

Acquisition

The Pflege Acquisition can be broken down into

the following three legs:

Acquisition of 39% shareholding of Pflege by EaseMyTrip,

which is an overseas entity, from Mr. Bhisham Sheoran

(“ODI Secondary”), Primary investment by EaseMyTrip into Pflege for

10.03% shareholding of Pflege (“ODI

Primary”), and Payment of consideration by EaseMyTrip to Mr. Bhisham

Sheoran1 and Pflege in the form of allotment

of its own shares (“FDI Primary”).

Based on the above, the Pflege Acquisition has

two forms of Share Swaps: an

ODI Primary –

FDI Primary Share Swap and an

ODI Secondary –

FDI Primary Share Swap.

2.

Jeewani

Acquisition

The Jeewani Acquisition can be broken down into

the following two legs:

Acquisition of 50% shareholding of Jeewani, an Indian

company, by EaseMyTrip, Payment of consideration to Jeewani in the form

of allotment of its own shares.

Based on the above, the Jeewani Acquisition has

one form of Share Swap:

Resident –

Resident Share Swap.

3.

Planet

Acquisition

The Planet Acquisition can be broken down into

the following two legs:

Acquisition of 49.03% shareholding of Planet by

EaseMyTrip, which is an overseas entity, from Mr.

Gagandeep Singh and Mr. Sanket Champaklal Shah (“Planet

ODI Secondary”), Payment of consideration by EaseMyTrip Mr. Gagandeep

Singh and Mr. Sanket Champaklal Shah2

in the form of allotment of its own shares (“Planet

FDI Primary”).

Therefore, the Planet Acquisition has one form

of Share Swap: an

ODI Secondary –

FDI Primary Share Swap.

LEGAL CONSIDERATIONS APPLICABLE

TO SHARE SWAPS

Each of EaseMyTrip’s acquisitions constitute

differing forms of Share Swaps. Share Swaps must

meet a variety of requirements under major Indian

legislations such as merger control laws, tax laws,

foreign exchange control laws, company law, etc.

Further, given that each of these Share Swaps

include EaseMyTrip, which is a listed company, laws

governing listed securities enacted by the Securities

and Exchange Board of India (“SEBI”)

also get triggered.

Let us now delve into an assessment of the laws

typically applicable to Share Swaps, and how each

of them is being specifically triggered in EaseMyTrip’s

acquisitions.

1.

Foreign

exchange control considerations:

Share Swaps involving non-resident shareholders

and / or companies will have to be undertaken in

compliance with the Foreign Exchange Management

Act, 1999 (“FEMA”)

and the allied regime enacted thereunder.

FEMA

Compliances

-

Compliance with the NDI Rules:

As mentioned above, each of the Pflege Acquisition

and Planet Acquisition have FDI Primary as a step

in their swaps. The Jeewani Acquisition is a domestic

share swap; therefore, the NDI Rules will not be

applicable to the same. The NDI Rules, as per Rule

6(a) read with Schedule I allows an Indian company

to issue equity instruments to a person resident

outside India against swap of equity instruments.

As per the NDI Rules, foreign direct investment

(“FDI”) into Indian

companies can occur without prior approval of the

Indian government so long as the Indian company

falls in the “automatic route” under

Schedule I of the NDI Rules. Therefore, if the Indian

company falls under the automatic route, then a

share swap would not require government approval.

The Pflege Acquisition consisted of an FDI Primary

wherein EaseMyTrip allotted its own shares to non-residents.

Similarly, the Planet Acquisition also consisted

of the Planet FDI Primary involving allotment to

non-resident individual shareholders of Planet.

However, since investments into the tourism sector

fall under the 100% automatic route, these transactions

did not need to factor in a potential requirement

for the prior approval of the Indian government

under the NDI Rules.

Prior approval under the Press

Note No. 3 (2020 Series) (“PN3”):

In addition to the NDI Rules, the parties may

have also had to evaluate whether any prior approval

of the Indian government is required under the PN3.

As per the PN3, prior government approval is required

in case of any FDI from entities of countries that

share land-borders with India, or where the beneficial

owner of an investment into India is situated in

or is a citizen of such land-bordering countries.

PN3 was enacted in 2020 to curb opportunistic investments

from China and other land bordering countries.3

The PN3 consideration is relevant for the Pflege

Acquisition and Planet Acquisition, since both of

them involve FDI into EaseMyTrip (in lieu of the

Share Swap). Accordingly, in case any of the proposed

allottees of EaseMyTrip’s shares in these

transactions (i.e. Pflege, Jeewani, Planet, Mr.

Bhisham Sheoran, Mr. Gagandeep Singh and Mr. Sanket

Champaklal Shah) are resident in / have beneficial

owners that are situated in land-bordering countries,

such allotment would be subject to government approval

under the PN3. Basis the publicly available information,

neither of the acquirers of the shares of EaseMyTrip

are resident of/have beneficial owners that are

situated in land-bordering countries.

2.

Overseas

investment law considerations:

The Pflege Acquisition and Planet Acquisition

involves issuance / transfer of shares of an unlisted

foreign company (amounting to more than 10% shareholding)

to an Indian company. Considering that Pflege and

Planet are unlisted foreign companies, the acquisition

of shares by EaseMyTrip constitutes an “overseas

direct investment” (“ODI”)

under the Foreign Exchange Management (Overseas

Investment) Rules, 2022 (“OI Rules”).4

Rule 11 read with Schedule I of the OI Rules

clarifies the mechanisms through which ODI can be

undertaken by Indian entities, which under Para

2 (v) of Schedule I, permits ODI by way of a ‘swap

of securities’. Accordingly, the Pflege Acquisition

and Planet Acquisition constitute permissible modes

of undertaking ODI under the OI Rules.

However, ODI is subject to certain additional

factors that also need to be met, namely –

Net

worth criteria

Thetotal financial commitment made by an Indian

entity in all the foreign entities, taken together

at the time of undertaking such commitment, shall

not exceed 400 percent of its net worth as on the

date of the last audited balance sheet.5

The total consideration for the Pflege Acquisition

and Planet Acquisition is INR 69,03,05,000. As per

the audited financial statements of EaseMyTrip for

FY 23-24, the net worth of EaseMyTrip is INR 637,90,90,000.6

Further, while the exact amount of financial commitment

by EaseMyTrip in foreign entities is not available

as on the proposed date of consummation of the Pflege

Acquisition and Planet Acquisition, we note from

the audited financial statements for FY 23-24 that

EaseMyTrip has no foreign investments.7

Accordingly, since the proposed investment does

not exceed 400 percent of EaseMyTrip’s net

worth as on the date of the audited financial statements

for FY 23-24, the first requirement under the OI

Rules is met.

Financial

services criteria

AnIndian entity that is engaged in “financial

services” activities in India can make ODI

into a foreign entity engaged directly or indirectly

in financial services only if –

the Indian entity has posted net profits during

the preceding three financial years;

the Indian entity is registered with or regulated

by a financial services regulator in India;

the Indian entity has obtained approval as may be

required from the regulators of such financial services

activity, both in India and the host country or

host jurisdiction, as the case may be, for engaging

in such financial services:

However, if the Indian entity is not engaged

in “financial services” and seeks to

invest in a foreign entity which is directly or

indirectly engaged in “financial services”8

activities, the Indian entity should have posted

net profits during the preceding three financial

years.

In respect of the above, the following two-fold

determination is to be made to determine whether

the Pflege Acquisition and Planet Acquisition must

meet the aforementioned criteria –

Is EaseMyTrip (being the Indian entity) engaged

in “financial services” activities?

Are the foreign companies in which EaseMyTrip is

undertaking ODI (namely, Pflege and Planet) engaged

directly or indirectly in “financial services”

activities?

With respect to (i) above, it is to be noted

that as per the Business Responsibility & Sustainability

Report of EaseMyTrip for FY 23-24, the NIC Code

for activities contributing to 100% of the turnover

of EaseMyTrip is 7911 (Tour and Travel related services).

Accordingly, it can be stated that EaseMyTrip is

not engaged in financial services activities in

India.

On the other hand, based on the disclosures made

by EaseMyTrip to stock exchanges and publicly available

information, Pflege is a home health care provider

based in Dubai, which offers medical tourism services

through licensed doctors around the globe, along

with supporting services such as visa assistance

and airport drop and pickups.9 Separately,

Planet provides students with guidance through their

admission processes to universities in Australia,

with a range of services such as counseling, course

selection, coaching, visa applications, etc.10

Therefore, it is safe to assume that each of the

foreign target companies are also not involved directly

or indirectly in “financial services”

activities.

3.

SEBI considerations:

The issuance and allotment of specified securities11

by listed companies is governed by the Securities

and Exchange Board of India (Issue of Capital and

Disclosure Requirements) Regulations 2018 (“ICDR”).

ICDR is applicable to the present scenario since

EaseMyTrip is a listed company.

The preferential allotment of such securities,

for consideration other than cash, must comply with

the following requirements:

Approval through special resolution:

Any issuance of specified securities must be

approved by the shareholders of the listed company

by way of a special resolution.12

Accordingly, prior to effectuating the Pflege

Acquisition / Jeewani Acquisition / Planet Acquisition,

EaseMyTrip must receive the consent of 75% of its

shareholders through a special resolution.

Valuation requirements:

Another equally important consideration is the

valuation requirement that is prescribed under the

ICDR. Consideration other than cash, discharged

by way of a swap of shares, should be backed by

a valuation report issued by an independent registered

valuer and submitted to the stock exchanges where

the issuer is listed. However, the stock exchanges

have the ability to get the valuation done by another

valuer in case they are not satisfied with the appropriateness

of the valuation.13

Therefore, the Share Swaps occurring pursuant

to each of the aforementioned acquisitions are required

to be justified through a valuation report issued

in respect of these transactions.

Pricing guidelines:

The pricing guidelines under Regulation 164 of

the ICDR are to be followed for a preferential issue

in case the shares of the issuer company are “frequently

traded”. The shares of an issuer company are

considered to be “frequently traded”

in case the equity shares of the issuer have been

listed on a recognized stock exchange for a period

of 90 trading days or more as on the “relevant

date” (which, for the purposes of these acquisitions

would be the date thirty days prior to the date

on which the meeting of shareholders is held to

consider the proposed preferential issue14).

Considering that EaseMyTrip’s shares are “frequently

traded”, the price of the equity shares to

be allotted must not be the higher of:

-

90 days’ volume

weighted average price of related equity shares

quoted on the recognized stock exchange preceding

the relevant date, or

-

10 trading days’

volume weighted average prices of related equity

shares quoted on a recognized stock exchange,

preceding the relevant date,15

unless the method of determination specified

in the articles of association provide a higher

floor price than the one that may be arrived at

using the aforementioned methods of calculation.

Other requirements for conducting preferential

issue:

Regulation 160 of the ICDR specified certain

other requirements that are also to be met prior

to conducting a preferential issuance, such as –

The securities being

issued must be fully paid-up; Equity shares held

by proposed allottees in the issuer, if any,

are in dematerialized form; An in-principle application

has been made to the stock exchange on the day

that a notice for the shareholders’ meeting

has been sent to the shareholders.

Pursuant to the valuation requirements set out

above, EaseMyTrip procured a valuation report from

Samarth Valuation Advisory LLP, a registered valuer,

for issuing a pricing certificate under the ICDR

(“Pricing Certificate”).

The Pricing Certificate: (i) assessed the fair value

of the equity shares as per internationally accepted

valuation standards of the Institute of Chartered

Accountants of India as on September 30, 2024; and

(ii) determined the floor price of shares as per

Chapter V of the ICDR on December 6, 2024. The Pricing

Certificate computed the fair value of shares to

be INR 16.66 and the floor price (as per the ICDR)

to be INR 18.22 per equity share.

Relying on the above, EaseMyTrip’s proposed

issue price towards the allottees pursuant to the

Pflege Acquisition, Jeewani Acquisition and Planet

Acquisition was INR 18.22 per share.

4.

Merger

control considerations:

Under the regime set out pursuant to the Competition

Act, 2002 (“Competition Act”),

transactions amounting to “combinations”

are notifiable (i.e. subject to the prior approval

of the Competition Commission of India (“CCI”))

if they cross the thresholds set out in Section

5 of the Competition Act.

That being said, under the Competition (Minimum

Value of Assets and Turnover) Rules, 2024, combinations

are exempt from mandatory prior notification to

the CCI if the target entity’s consolidated

assets or turnover, as per its latest audited financial

statements, fall below either of the following thresholds:

(i) assets of less than INR 450 crore (Indian Rupees

Four Hundred and Fifty Crores) in India; or (ii)

turnover of less than INR 1,250 crore (Indian Rupees

One Thousand Two Hundred and Fifty Crores) in India

(the “De Minimis Exemption”).

Interestingly, from September 10, 2024, the merger

control regime was overhauled and in addition to

the thresholds set out in Section 5 of the Competition

Act, the Competition Commission of India (Combination)

Regulations, 2024 (“Combination Regulations”)

were introduced, which brought in deal value threshold

(“DVT”). DVT is an

additional mechanism against which transactions

are required to assess the requirement of mandatory

notification to the CCI (over and above the Section

5 thresholds). As per the DVT, the following transactions

are notifiable (irrespective of the availability

of the De Minimis Exemption): (i) the value of the

transaction is INR 2,000 crores (i.e. approximately

USD 231 million) or more (“Value Test”);

and (ii) the target has “substantial business

operations” in India, each as per the manner

set out in the Combination Regulations.

A transaction would be exempt from notification

under the DVT only if it is able to avail any of

the exemptions set out under the Competition (Criteria

for Exemptions of Combinations) Rules 2024 (“General

Exemptions”).

Accordingly, any combination which either breaches

the thresholds under Section 5 or triggers the DVT

would be required to be mandatorily notified to

the CCI, unless such combination can either avail

the De Minimis Exemption (only in case the notifiability

is due to breach of thresholds under Section 5)

or the General Exemptions (in case the notifiability

is due to breach of thresholds under Section 5 or

trigger of DVT).

The proposed issuance of shares to the allottees

pursuant to each of the Pflege Acquisition, Jeewani

Acquisition and Planet Acquisition cumulatively

amounts to approximately INR 234,00,00,000 (Indian

Rupees Two Hundred Thirty Four Crores). Accordingly,

neither of these transactions (either individually

or when interconnected) cross the Value Test and

trigger the DVT.

Further, as per the audited financial statements

of EaseMyTrip for FY 23-24, the consolidated assets

amount to INR 893,61,30,000 (Indian Rupees Eight

Hundred Ninety Three Crore Sixty One Lakh Thirty

Thousand) and the consolidated turnover is INR 609,08,10,000

(Indian Rupees Six Hundred Nine Crore Eight Lakh

Ten Thousand).16 Accordingly, EaseMyTrip

will be able to avail the De Minimis Exemption for

each of the Pflege Acquisition, Jeewani Acquisition

and Planet Acquisition.

5.

Tax considerations:

Pflege Acquisition: For the purposes

of the ODI Secondary as part of the Pflege Acquisition,

the shareholder Mr. Brishram Sheoran will be taxable

as per the tax laws of his jurisdiction of residence

for the gains derived by him as part of the Acquisition.

Jeewani Acquisition: Given that the

entire Jeewani Acquisition is structure as a primary

swap, there shall be no taxable event at the time

of Share Swap of Jeewani Acquisition.

Planet Acquisition: For the purposes

of Planet ODI Secondary as part of the Planet Acquisition,

the gains derived by Mr. Gagandeep Singh and Mr.

Sanket Champaklal Shah as part of the sale of the

shares held by them in Planet will be taxable as

per the tax laws of his jurisdiction of residence.

6.

Company

law considerations:

Under the Companies Act, 2013 (“Companies

Act”) read with ancillary

regulations, the power of further issuance of share

capital stems from Section 42 read with Section

62. Section 62 (1) (c) specifically deals with the

issuance of securities for consideration other than

cash. The critical requirements to be met for non-cash

share swaps under the Companies Act are as follows –

Approval through special resolution:

Similar to the ICDR, the issuance must be approved

by the shareholders through a special resolution. Valuation requirements:

The price of the shares must be determined by

a valuation report issued by an independent valuer,17

as evidenced by the Pricing Certificate.

Are

Pflege, Planet and Jeewani a “subsidiary company”

of EaseMyTrip under the Companies Act?

As set out above, pursuant to the Share Swaps,

EaseMyTrip intends to acquire nearly half of the

total shareholding in Pflege, Planet and Jeewani.

An interesting consideration that therefore emerges

is as to whether these companies are its subsidiaries

under the Companies Act, and if not, whether there

is any reason why?

Under Section 2(87) of the Companies Act, a company

becomes a “subsidiary company” if either

of the following conditions are met: (i) the holding

company controls the composition of the board of

directors; or (ii) the holding company exercises

/ controls more than half of the total voting power,

either by itself or through one or more subsidiary

companies.

As per the disclosure made by EaseMyTrip on the

stock exchanges on December 7, 2024, it appears

that there is no board seat that is being acquired

on the board of any of the three companies. Thus,

part (i) of the definition of “subsidiary

company” does not apply. Further, EaseMyTrip

is not acquiring more than 50% shareholding in any

of the companies. Since this leads to a situation

where it cannot exercise “more than half

of the total voting power” in these companies,

part (ii) of the definition is also not met. Accordingly,

Pflege, Planet and Jeewani are not subsidiary companies

of EaseMyTrip.

However, the question still remains – would

this have been a deliberate move?

Looks like at-least for Jeewani it would be.

According to Section 19 of the Companies Act, a

subsidiary company

cannot

hold any shares in its holding company except

in the case where such subsidiary company holds

the shares of its holding company (a) as the legal

representative of a deceased member of the holding

company or (b) as a trustee or (c) even before it

became a subsidiary company of the holding company.

Further, holding companies are restricted from allotting

or transferring their shares to any of its subsidiary

companies.

If EaseMyTrip would have acquired more than half

of the total voting power in Jeewani, this company

would have become a “subsidiary company”

of EaseMyTrip under the Companies Act and the share

swap would not be possible because of the restriction

set out in Section 19 of the Companies Act. Thus,

it is possible that the total shareholding acquired

in Jeewani pursuant to the Share Swap was decided

keeping this consideration in mind.

SES’ RECOMMENDATIONS AGAINST

THE SHARE SWAPS

As mentioned above, under Regulation 160 of the

ICDR, preferential issuances by listed companies

are required to be approved by a special resolution

of the shareholders. Institutional and retail shareholders

alike often place reliance on the reports and recommendations

of proxy advisors to understand the implications

of such corporate actions.

In this regard, on January 07, 2025, SES released

a report with its recommendations to shareholders

in respect of the proposed preferential allotment

of shares of EaseMyTrip (which included the issuances

pursuant to the Pflege Acquisition, Jeewani Acquisition

and Planet Acquisition).

The agenda being proposed by EaseMyTrip was seeking

shareholders’ approval towards primary issuances

of equity shares of EaseMyTrip to each of Pflege,

Jeewani, Planet, Mr. Bhisham Sheoran, Mr. Gagandeep

Singh, and Mr. Sanket Champaklal Shah, on a non-cash

basis (collectively, the “Non-Cash

Allotment”). Along with these issuances,

they had also sought shareholders’ approval

for allotment of equity shares to Ms. Jacqueline

Genevieve Fernandes on a cash basis (the “Cash

Allotment”). Each of these are non-promoter

individuals.

The total size of issue was 12,84,47,034 (Twelve

Crore Eighty Four Lakh Forty Seven Thousand Thirty

Four) fully paid-up equity shares having a face

value of INR 1 each, at an issue price of INR 18.22

per share that collectively took the issue size

to approximately INR 234,00,00,000 (Indian Rupees

Two Hundred Thirty Four Crores).

Broadly, the proxy advisor had two major observations

whilst analyzing the aforesaid transaction:

The potential dilution in EaseMyTrip would cumulatively

amount to 3.49% (with the Cash Allotment constituting

a mere 0.07% dilution of the existing shareholders’

shareholding); and

Although the valuation report obtained for the Non-Cash

Allotment and Cash Allotment refers to the consideration

of a “fair equity share swap ratio”

it only provides a price determination for EaseMyTrip’s

shares and does not separately account for the valuation

/ information of Pflege, Jeewani, or Planet.

Non-Cash Allotment

SES referred to Rule 13(2)(d) of the Companies

(Share Capital and Debentures) Rules, 2014 and Rule

163(3) of the ICDR to note that in case of the allotment

of securities for consideration other than cash,

a justification of the valuation must be provided

pursuant to a “valuation report”

from a registered valuer.

The proxy advisor had the following specific

observations in relation to the valuation report –

They referred to the language set out in the aforesaid

regulations and noted that considering that the

Non-Cash Allotment involves an underlying transaction

of a share swap, the valuation report of the target

companies should also be provided to the shareholders.

Further, since the valuation report of Pflege, Jeewani

and Planet were not provided, SES referred to the

last year revenue information of these companies

to note that the stakes being acquired were significantly

lesser than the consideration being paid to the

shareholders of Planet, Jeewani and Pflege through

the share swap.

Accordingly, SES was of the view that the valuation

was not providing shareholders with a clear picture

to gauge the value of the consolidated proposed

acquisitions, making the valuation unfair and non-transparent.

Further, they noted that the proposed dilution of

shareholding in EaseMyTrip was also not adequately

justified due to the above factors.

Thus, they recommended voting against the Non-Cash

Allotment on account of a “compliance concern”.

Cash Allotment

With respect to the Cash Allotment, SES noted

that since the shares were being issued in lieu

of cash, the aforementioned concerns with respect

to valuation would not arise (as there is no involvement

of the target companies in this transaction). Additionally,

the cumulative dilution as a result of the Cash

Allotment was noted to be insignificant.

Therefore, no concerns were raised with respect

to the Cash Allotment.

CONCLUSION

The EaseMyTrip Share Swaps highlight the growing

role of non-cash structures in corporate expansion.

While the deals align with EaseMyTrip’s vision

for diversification and inorganic growth, the complex

regulatory landscape surrounding foreign exchange

laws, SEBI regulations, tax implications, and merger

control adds layers of compliance, which will have

to be borne in mind by dealmakers across the industry

at the time of structuring similar Share Swaps.

In addition to a complex array of laws that need

to be navigated whilst structuring Share Swaps,

specifically in the case of listed companies, dealmakers

will also have to be wary of other stakeholders

such as proxy advisory firms and ensure that factors

such as valuation transparency and shareholder dilution

concerns are adequately resolved to ensure greater

disclosure and justification in share swap transactions.

Authors

-

Anurag Shah,

Parina Muchhala and

Nishchal Joshipura

You can direct your queries or comments to the relevant member.

1Based on the assumption that Mr.

Bhisham Sheoran will be a non-resident under the

Foreign Exchange Management Act, 1999.

2Based on the assumption that Mr.

Gagandeep Singh and Mr. Sanket Champaklal Shah will

be non-residents under the Foreign Exchange Management

Act, 1999. It appears that they are both based currently

in Australia, as available at:

https://www.planeteducation.info/our-team.

3Available at:

https://dpiit.gov.in/sites/default/files/pn3_2020.pdf.

4As per the OI Rules, “Overseas

Direct Investment” or “ODI”

means

investment by way of acquisition of unlisted equity

capital of a foreign entity, or

subscription as a part of the memorandum of association

of a foreign entity, or investment in ten per cent,

or more of the paid-up equity capital of a listed

foreign entity or investment with control where

investment is less than ten per cent. of the paid-up

equity capital of a listed foreign entity.

5Para 3 (1), Schedule I of the OI

Rules.

6https://www.bseindia.com/xml-data/corpfiling/AttachHis/021a2e21-36c8-4236-b44d-b60647883660.pdf.

7Please refer to “Note No. 10”

of the “Notes to Accounts” of the Consolidated

Financial Statements of EaseMyTrip for FY 23-24.

8As per Schedule I, a foreign entity

shall be considered to be engaged in the business

of financial services activity if it undertakes

an activity, which if carried out by an entity in

India, requires registration with or is regulated

by a financial sector regulator in India.

9https://pflegehealthcare.com/about-us.

10https://www.planeteducation.info/international-education.

11Under the ICDR, “specified

securities” means equity shares and convertible

securities.

12Regulation 160 (b), ICDR.

13Regulation 163 (3), ICDR.

14Regulation 161 a), ICDR.

15Regulation 164 (1), ICDR.

16https://www.bseindia.com/xml-data/corpfiling/AttachHis/021a2e21-36c8-4236-b44d-b60647883660.pdf.

17Section 62 (1) (c), Companies Act.

Disclaimer

The contents of this hotline should

not be construed as legal opinion. View detailed disclaimer.

This hotline does not constitute a

legal opinion and may contain information generated

using various artificial intelligence (AI) tools or

assistants, including but not limited to our in-house

tool,

NaiDA. We strive to ensure the highest quality and

accuracy of our content and services. Nishith Desai

Associates is committed to the responsible use of AI

tools, maintaining client confidentiality, and adhering

to strict data protection policies to safeguard your

information.

This hotline provides general information

existing at the time of preparation. The Hotline is

intended as a news update and Nishith Desai Associates

neither assumes nor accepts any responsibility for any

loss arising to any person acting or refraining from

acting as a result of any material contained in this

Hotline. It is recommended that professional advice

be taken based on the specific facts and circumstances.

This hotline does not substitute the need to refer to

the original pronouncements.

This is not a spam email. You have

received this email because you have either requested

for it or someone must have suggested your name. Since

India has no anti-spamming law, we refer to the US directive,

which states that a email cannot be considered spam

if it contains the sender's contact information, which

this email does. In case this email doesn't concern

you, please

unsubscribe from mailing list.

|

|

We aspire

to build the next generation

of socially-conscious lawyers

who strive to make the world

a better place.

At NDA, there

is always room for the right

people! A platform for self-driven

intrapreneurs solving complex

problems through research, academics,

thought leadership and innovation,

we are a community of non-hierarchical,

non-siloed professionals doing

extraordinary work for the world’s

best clients.

We welcome

the industry’s best talent -

inspired, competent, proactive

and research minded- with credentials

in Corporate Law (in particular

M&A/PE Fund Formation),

International Tax , TMT and

cross-border dispute resolution.

Write to

[email protected]

To learn more

about us

Click here.

|

|

Chambers

and Partners Asia

Pacific 2025:

Top Tier for Tax,

Technology Media

and Telecoms (TMT),

Life Sciences, Dispute

Resolution, Private

Equity, Corporate/M&A:

The Elite, White-Collar

Crime & Corporate

Investigations,

Investment Funds,

FinTech, Cross-Border

Capabilities, High

Net Worth Guide

and Private Wealth

Law.

Legal 500

Asia Pacific 2024:

Top Tier for Tax,

TMT, Life Sciences

and Healthcare,

Dispute resolution:

arbitration, Dispute

resolution: litigation,

Data protection,

Fintech and financial

services regulatory,

Private equity funds

(including venture

capital), Labour

and employment,

Corporate and M&A

and Intellectual

Property.

Benchmark

Litigation Asia

Pacific 2024:

Top Tier for International

arbitration, Tax,

Labor and employment,

Commercial and transactions,

Government and regulatory,

Insolvency and Construction.

AsiaLaw

2024: Top

Tier for Tax, TMT,

Investment Funds,

Private Equity,

Labour and Employment,

Dispute Resolution,

Regulatory, Pharma

Asian Legal

Business (Thomson

Reuters) Pan Asian

Regulatory Summit

Awards 2024:

Top Regulatory Firm

across North and

South Asia.

Who’s

Who Legal 2025:

Global Thought Leaders

in Arbitration,

Sports & Gaming,

Private Funds and

Transport.

India Business

Law Journal’s

2024 Law Firm Awards:

Winner Law Firm

for Data Compliance &

Cybersecurity, Internet &

e-Commerce, Pharma &

Life Sciences and

Taxation (Direct).

ITR World

Tax Firm Rankings

2025: Top

Tier for General

corporate tax practice.

IFLR1000

2025: Top

Tier for M&A

and Private Equity.

FT Innovative

Lawyers Asia Pacific

2019 Awards:

NDA ranked 2nd in

the Most Innovative

Law Firm category

(Asia-Pacific Headquartered).

RSG-Financial

Times:

India’s Most

Innovative Law Firm

2019, 2017, 2016,

2015, 2014.

|

|

|

|